Types of differences and why they appear

Timing difference

Timing differences are those differences between accounting income and taxable income which can be reversed in one or more subsequent periods. For example, Depreciation allowed as per WDV method for computing taxable income and as per SLM method for computing accounting income.

Permanent difference

Permanent differences are those differences between accounting income and taxable income which cannot be reversed any subsequent period. For example, Donation paid in cash is disallowed in computing taxable income whereas it is allowed as expenditure while computing accounting income. There can be differences between accounting income and taxable income because of the following reasons :

1. Expenses debited in profit and loss statement, but disallowed as per Income Tax Act 1961, while computing taxable income

2. Provision for Bad/doubtful debts allowed while computing accounting income, but disallowed while computing taxable income

3. Charging depreciation using different rates as per Companies Act 2013 and Income Tax Act 1961

4. Any income recognized on an accrual basis in profit and loss statement but recognized on receipt basis in subsequent period for computing taxable income. In order to account for these kinds of differences, AS 22 needs to be applied.

When to apply AS 22 Accounting for Taxes on Income

AS 22 needs to be applied when there are differences between taxable income and accounting income. If taxable income is greater than accounting income, then it will result in deferred tax asset. And if accounting income is greater than taxable income, then it will result in deferred tax liability.

When the difference is resulting in deferred tax asset, then it should be recognized only when there is a reasonable certainty of its realization. The recognition of deferred tax asset should be to the extent of the reasonable certainty of the expected realization. The reasonable certainty can be determined by making the realistic estimates of future profits based on the examination of profits and loss statement of earlier periods.

Say, an entity has unabsorbed depreciation or carry forward of losses. In such a case, deferred tax asset should be recognized to the extent there is a virtual certainty supported by convincing evidence. Virtual certainty is a matter of judgment of convincing evidence, which should be available in a concrete form at a particular date.

How to apply AS 22 Accounting for Taxes on Income

The application of AS 22 can be explained with the help of examples: Example of timing difference:

| Particulars | Year 1 | Year 2 | Year 3 |

| Profit before tax (A) | 100,000 | 200,000 | 180,000 |

| Depreciation as per Companies Act (B) | 25,000 | 25,000 | 25,000 |

| Accounting income (A-B) | 75,000 | 175,000 | 125,000 |

| Depreciation as per Income tax Act (C) | 50,000 | 0 | 10,000 |

| Taxable income (A-C) | 50,000 | 200,000 | 170,000 |

| Timing difference (D) | 25,000 | -25,000 | -15,000 |

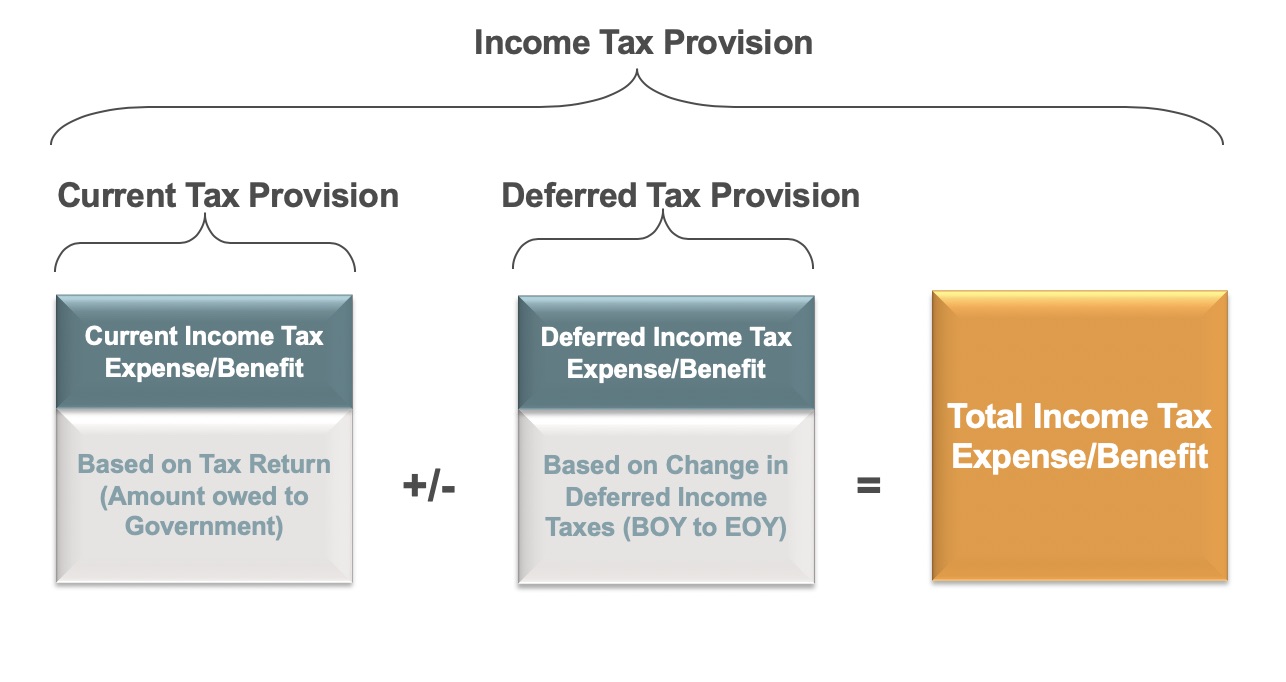

| Current tax @ 30% | 15,000 | 60,000 | 51,000 |

| Deferred tax (D * 30%) | 7,500 | -7,500 | -4,500 |

| Total tax expense | 22,500 | 52,500 | 46,500 |

| Profit after tax | 52,500 | 122,500 | 78,500 |

Deferred tax computation

| Particulars | Year 1 | Year 2 | Year 3 |

| Opening balance of timing difference | 0 | 25,000 | 0 |

| Addition | 25,000 | 0 | 15,000 |

| Deletion | 0 | 25,000 | 0 |

| Closing balance of timing difference | 25,000 | 0 | 15,000 |

| Deferred tax @ 30% | 7,500 | 7,500 | 4,500 |

| DTA/DTL | Creation of DTL | Reversal of DTL | Creation of DTA |

| Journal Entry | P&L A/c Dr. To DTL | DTL Dr. To P&L A/c | DTA Dr. To P&L A/c |

Comparison between AS 22 and IND AS 12

|

Basis |

AS 22 Accounting for Taxes on Income | IND AS 12 (Income taxes) |

|

Recognition |

AS 22 recognized tax effect of differences between taxable income and accounting income. | IND AS 12 recognized tax effect of differences between assets and/or liabilities and their tax base. |

|

Approach |

AS 22 is based on profit or loss statement approach. | IND AS 12 is based on balance sheet approach. |

|

Differences |

The types of differences on which AS 22 is applied are timing differences and permanent differences. | The types of differences on which IND AS 12 is applied are taxable temporary differences and deductible temporary differences. Permanent differences are not dealt in by this standard. |

|

Recognition of Deferred tax asset/deductible temporary differences |

DTA is recognized only when and to the extent there is a reasonable certainty of its realization | Deductible temporary differences are recognized to the extent of the probability of taxable profits in future periods. |

|

Disclosure |

AS 22 deals with the disclosure of DTA/DTL in the balance sheet. | IND AS 12 deals with the recognition of current or deferred tax as income or expense in profit and loss statement. It also deals with the disclosure of out of profit and loss transaction in the balance sheet as current or non-current assets/liability. |

|

Revaluation of assets |

AS 22 does not cover the difference arising between taxable income and accounting income due to the revaluation of assets. | IND AS 12 deals with the difference between carrying the amount of revalued asset and its tax base. |

|

Goodwill |

AS 22 does not cover the difference arising due to goodwill arising a business combination. | As per IND AS 12, the difference between carrying the amount of goodwill and its tax base (which will be NIL) is the taxable temporary difference. It does not allow the recognition of such difference because goodwill is measured as a residual and its recognition would increase the carrying amount of goodwill. |

|

The concept of virtual certainty |

When an entity has unabsorbed depreciation or carry forward of losses then in such a case deferred tax asset should be to the extent there is a virtual certainty supported by convincing evidence. | There is no concept of virtual certainty in IND AS 12. Deductible temporary differences are recognized to the extent of the probability of taxable profits in future periods. |

|

Tax holiday |

AS 22 specifically provides guidance regarding recognition of deferred tax in the situations of Tax Holiday under Sections 80-IA, 80-IB, 10A and 10B of Income-tax Act. | IND AS 12 does not specifically deal with the situations of the tax holiday. |

|

Capital Loss |

AS 22 provides guidance regarding recognition of DTA in case of loss under the head of ‘capital gains’. | IND AS 12 does not specifically provide for the same. |

IFRIC 23

IFRIC 23 also provides for Uncertainty over Income Tax Treatments. It requires an entity to treat uncertain tax treatments depending on which method will be best suited for its resolution. The major difference between AS 22 and IFRIC 23 is that IFRIC 23 requires an entity, while determining the current and deferred income tax assets and liabilities, to make an assessment whether it is probable that taxation authority will accept an uncertain tax treatment.

If it is not probable, then entity should reflect that uncertainty through either expected value approach or most likely approach. IFRIC 23 will be applicable for annual reporting periods beginning on or after 01.01.2019.

Frequently Asks Questions

Yes, bookkeeping can be done totally online leaving behind any window of errors or miscalculations.

Audit of accounts is compulsory by a Chartered Accountant for the following persons

| Tax Payer | Compulsory Audit required when |

|---|---|

| A person carrying on Business | If total sales, turnover or gross receipts are more than Rs. 1 crore |

| A person carrying on Profession | If gross receipts are more than Rs. 50 lakh |

| A person covered under presumptive income scheme section 44AD | If income of the business is lower than the presumptive income calculated as per Section 44AD and the person’s total income is more than the maximum income which is exempt from tax. |

| A person covered under presumptive income scheme section 44AE | If income of the business is lower than the presumptive income calculated as per Section 44AE. |

| A person covered under presumptive income scheme section 44ADA | If income of the profession is lower than the presumptive income calculated as per section 44ADA and the person’s total income is more then the maximum income which is exempt from tax. |

Don’t worry!! Our expert will help you to choose a best suitable plan for you. Get in touch with our team to get all your queries resolved. Write to us at info@finxurance.com or call us @+91 9643 203 209.